Method B: Single Library Source Fund

This method of handling a deposit account uses a single library source fund for the deposit account, and is similar to Method A. This method differs, however, by giving the deposit account its own appropriation (whereas method A funds the deposit account via a negative expenditure). As the vendor supplies items, you can expend them against the deposit account, thus decreasing the remaining balance. For further information on the fund balances, see Understanding the Balances in Fund Accounts Using Method B.

Example Funds

To show how this method works, the examples below use "govpb" to represent the source fund and "dpgpo" to represent the deposit account fund.

To set up the funds using this method, do the following.

- Create a fund to use as the source fund if one doesn't already exist. You will use this fund later for the appropriation of the deposit account fund.

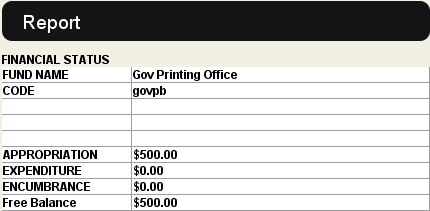

For example, if you create the source fund with an appropriation of $500.00, the initial fund report displays as follows.

- Create a fund for the deposit account if one doesn't already exist. Innovative recommends creating mnemonic codes like "dpgpo", with the beginning portion indicating it is a deposit account, for example, "dp", and the end portion specifying the vendor, for example, "gpo" for the U.S. Government Printing Office.

- Using the Fund Adjustment Table, enter a negative adjustment to the appropriation of the source fund (govpb) equal to the amount of the prepayment sent to the vendor. When you are finished, enter a positive adjustment in the same amount to the appropriation of the deposit account fund (dpgpo).

If your prepayment to the vendor is $100.00, your fund reports display as follows after the fund adjustments.

| govpb (source fund) | dpgpo (deposit account fund) | ||||

| Appropriation | Expenditure | Free Balance | Appropriation | Expenditure | Free Balance |

| $400.00 | $0.00 | $400.00 | $100.00 | $0.00 | $100.00 |

After you have finish setting up your funds, you can begin ordering items from the vendor. When you enter orders, use the deposit account fund in the order record. As items are received, you can process them using the invoicing functions.

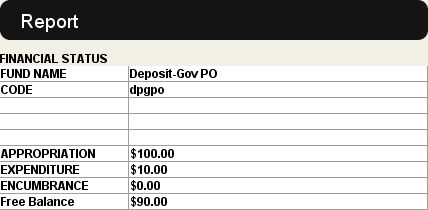

For example, if you process an item for $10.00, the fund report for the deposit account fund shows:

Understanding the Balances in Fund Accounts Using Method B

Just as with Method A, the balance of the general (source) fund is the actual cash amount remaining in the library's possession. The deposit account balance is the amount of credit left with the vendor. If you produce a fund report with a total for both balances, that total reflects the library's true assets, that is, those in its own cash account AND those which the vendor is holding in anticipation of orders for material.